Ethereum (ETH). is one network, but it can take different faces: it is a payment system, a place where stablecoins or non-convertible NFT tokens are developed. Glassnode in its latest analysis calls Ethereum a “decentralized general-purpose computer”, which corresponds to the original vision of its founders. The article is a continuation of the post on which parts of the Ethereum network are the most popular. In this section, we will look at each of the major categories separately. In the article you will learn, among other things:

Table of Contents

Vanilla, or Ethereum, typically used as a currency

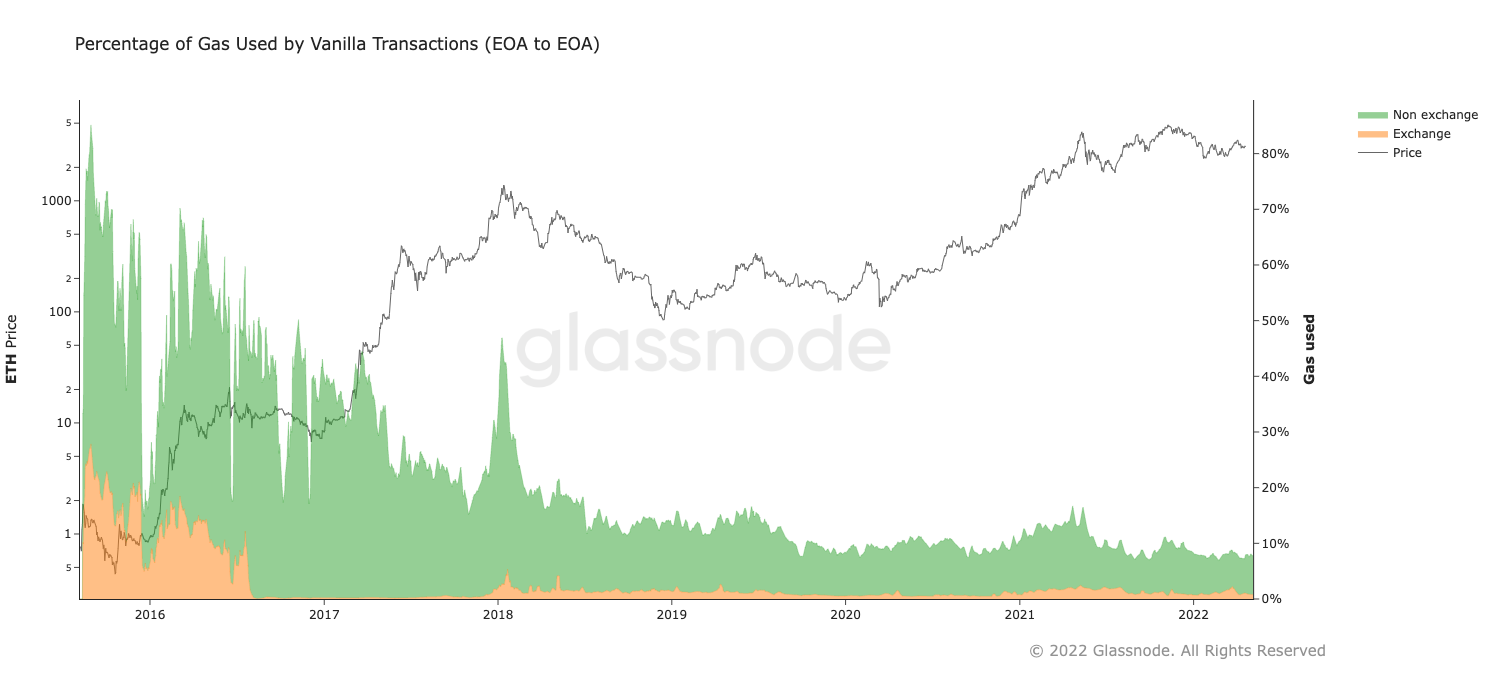

Conceptually, vanilla transfers represent ETH in the form of currency. From a gas consumption perspective, this form of use has declined from the most predominant level in the initial period (80% of gas in 2015) to a range of around 10% in the last two years. In other words: empirically, the Ethereum network is not primarily – or even largely – used to pass ETH between users.

Percentage of gas used by vanilla transactions. Source: Glassnode It would be a mistake, however, to assume that the Ethereum blockchain currently records fewer transactions in ethers than in 2016. The reason for this is repeatedly increasing gas limits in history. When Ethereum first took off in 2015, the gas cap was 5,000 units per block. It has since gradually grown to a target of 15 million blocks – and could be twice as high during periods of network congestion following the London update. Thus, while the relative importance of ETH transfers has decreased over time, absolute throughput has increased by many orders of magnitude.

Percentage of gas used by vanilla transactions. Source: Glassnode It would be a mistake, however, to assume that the Ethereum blockchain currently records fewer transactions in ethers than in 2016. The reason for this is repeatedly increasing gas limits in history. When Ethereum first took off in 2015, the gas cap was 5,000 units per block. It has since gradually grown to a target of 15 million blocks – and could be twice as high during periods of network congestion following the London update. Thus, while the relative importance of ETH transfers has decreased over time, absolute throughput has increased by many orders of magnitude.

You can invest in cryptocurrencies in the form of CFDs with, among others, the Plus500 broker. Create an account and start trading!

I WANT TO TRADE CFDs ON CRYPTOCURRENCY 77% of retail investor accounts lose money when trading CFDs with this provider. Consider whether you can afford the high risk of losing your money

Stablecoins

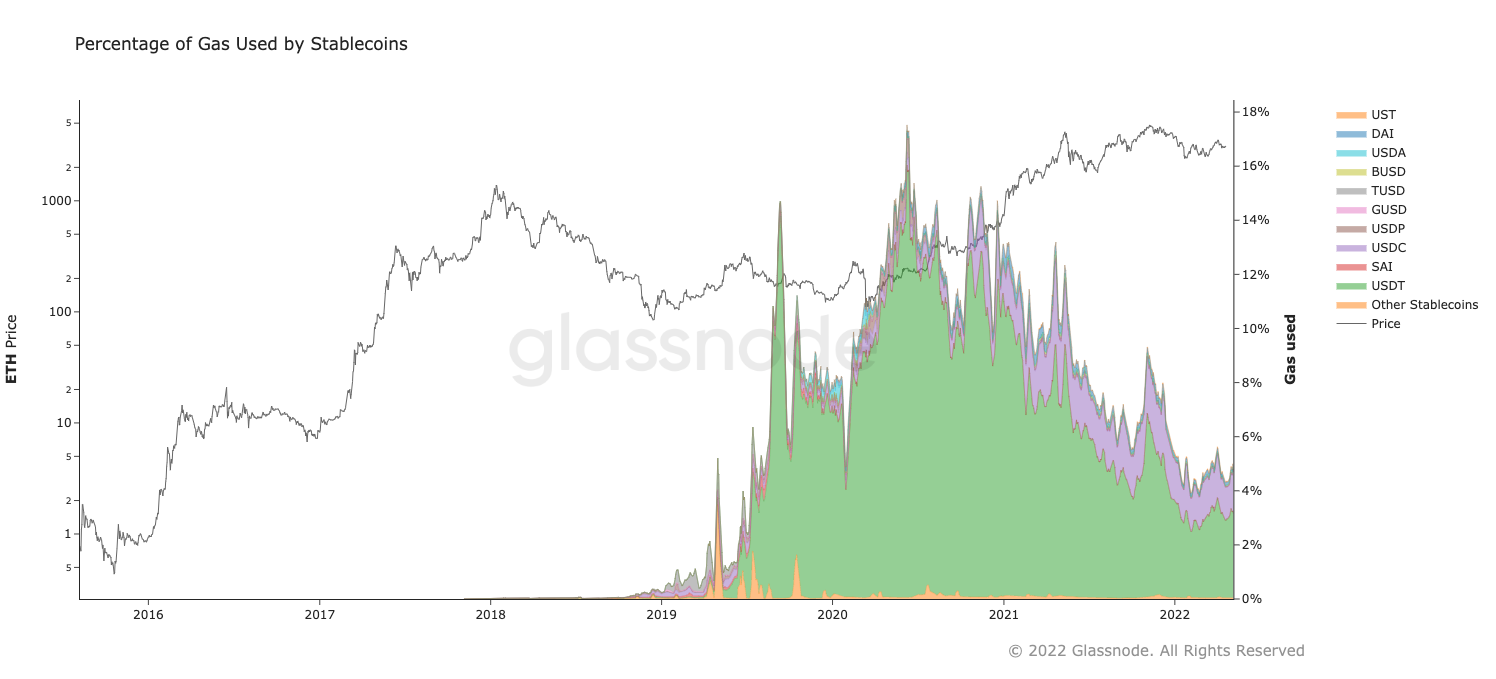

Stablecoins were not born on Ethereum, but this is where they first flourished. Initiated by Tether (USDT) migrating from Bitcoin (BTC) in search of lower fees and faster confirmation times, stablecoins have quickly become a powerhouse in terms of gas consumption. Over the past three years, most of the time, Ethereum has been used more as a payment platform for dollars than for ETH, with as of late 2019 monthly stablecoin transfer volumes are higher than ether each month.

The percentage of gas used by stablecoins. Source: Glassnode In addition to USDT, in the rapidly expanding space of stablecoins there is increasing competition for both centralized (USDT and USDC) and algorithmic (peg maintained by an incentive structure such as DAI and UST) projects. However, the dynamics of this competition cannot be inferred from the chart above. As fiat-denominated fees on Ethereum became a problem, stablecoins expanded their activities to other blockchains. Currently, more USDT has been issued on the Tron platform than on Ethereum. USDC supports 8 different blockchains. To the extent that Ethereum is used as a general-purpose decentralized computer, it may still lose market share to competing platforms that are cheaper or faster, or both.

The percentage of gas used by stablecoins. Source: Glassnode In addition to USDT, in the rapidly expanding space of stablecoins there is increasing competition for both centralized (USDT and USDC) and algorithmic (peg maintained by an incentive structure such as DAI and UST) projects. However, the dynamics of this competition cannot be inferred from the chart above. As fiat-denominated fees on Ethereum became a problem, stablecoins expanded their activities to other blockchains. Currently, more USDT has been issued on the Tron platform than on Ethereum. USDC supports 8 different blockchains. To the extent that Ethereum is used as a general-purpose decentralized computer, it may still lose market share to competing platforms that are cheaper or faster, or both.

ERC-20, i.e. universal use in the case of interchangeable tools

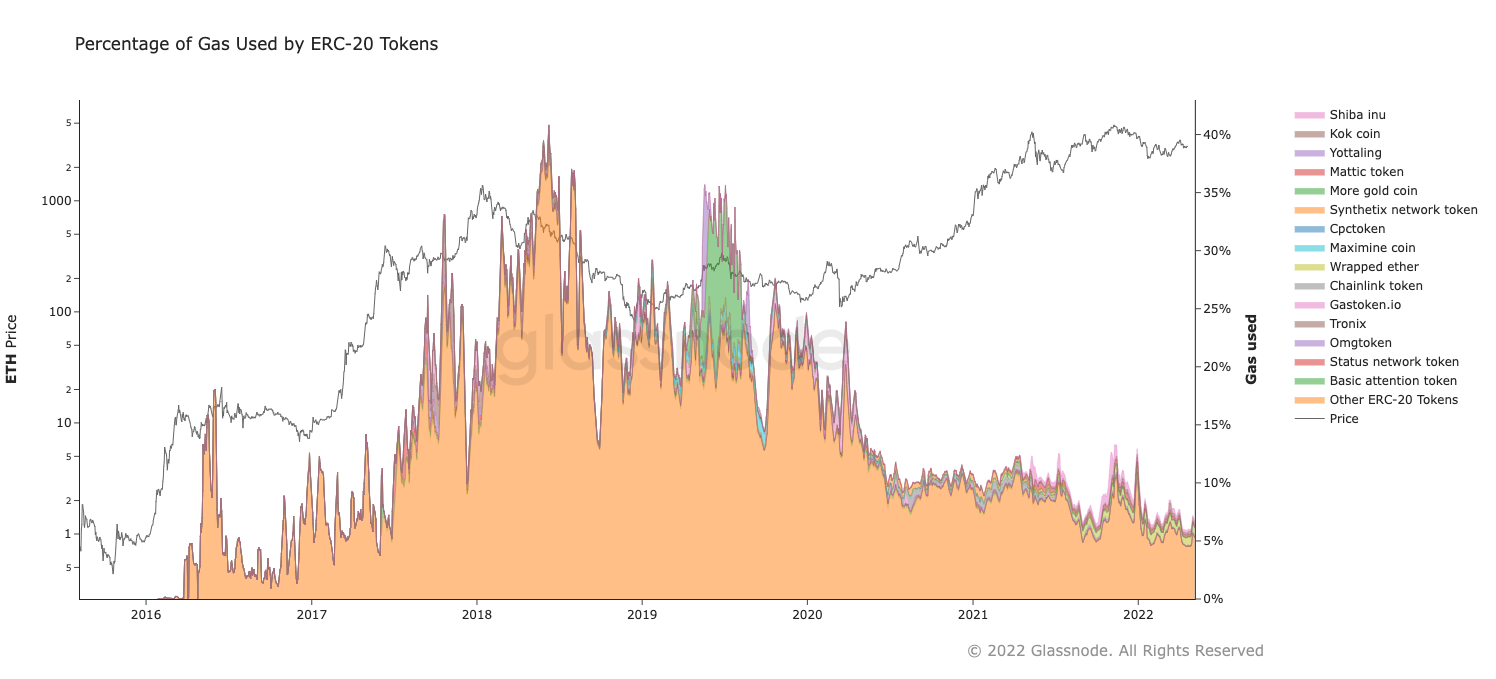

For fungible tokens, most of which are implemented as ERC-20 contracts, 40% of the gas market share in 2018 was a historic peak. The times of ICO frenzy seem to be behind us, and over the past few years, the share of this use case in the gas market has been modest at 5-10%. The chart shows the dominance of the subcategory “other ERC-20 tokens”. Many projects have had 15 minutes of fame in history, and at any point in time this category is dominated by several hits of the month.

Percentage of gas used by ERC-20 tokens. Source: Glassnode Even if we look at the most popular tokens in history, none of them dominate for more than one year. A notable subcategory of convertible tokens are wrapped assets, in particular WETH and WBTC, which enable the transfer of tokens to native tokens of the respective chains and decentralized use cases in finance.

Percentage of gas used by ERC-20 tokens. Source: Glassnode Even if we look at the most popular tokens in history, none of them dominate for more than one year. A notable subcategory of convertible tokens are wrapped assets, in particular WETH and WBTC, which enable the transfer of tokens to native tokens of the respective chains and decentralized use cases in finance.

DeFi. Decentralized finance

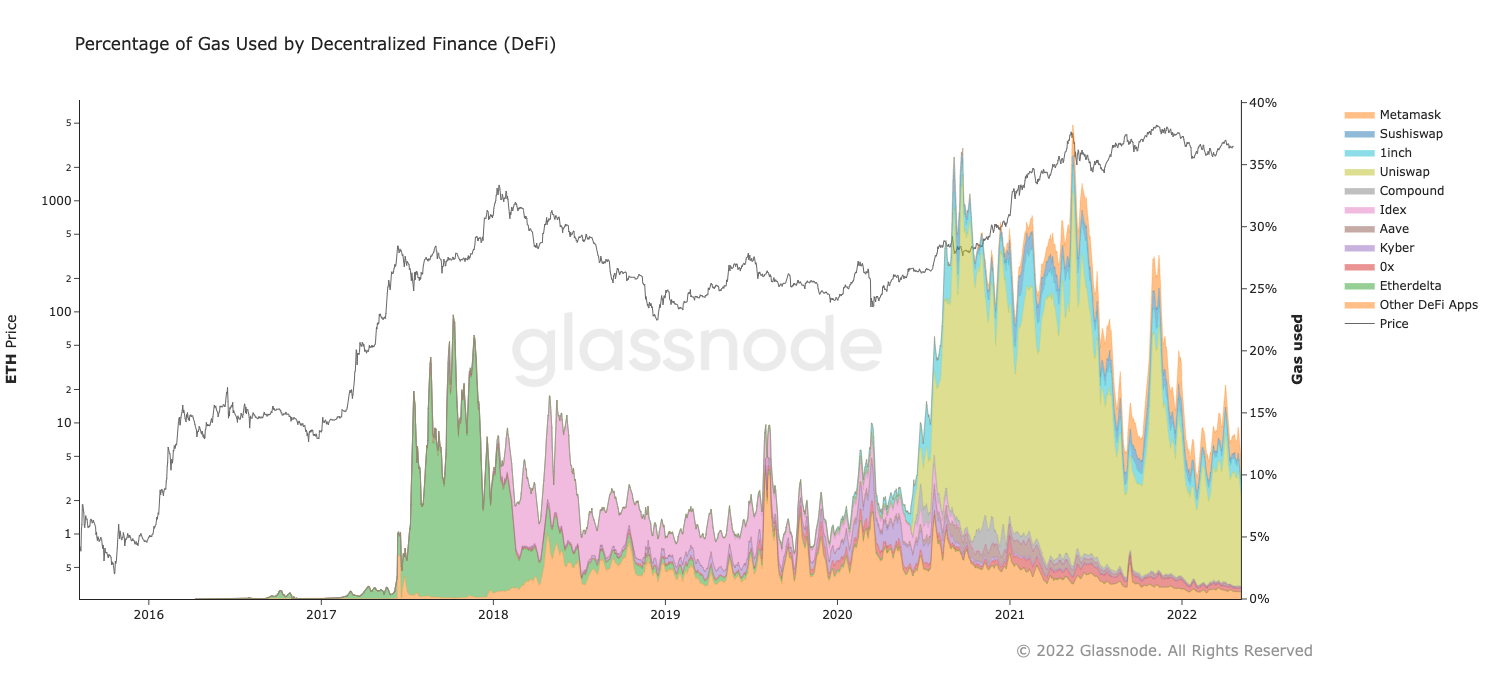

There are many uses for decentralized finance (DeFi) – lending, borrowing, trading in the spot market and derivatives, earning interest, insurance and more. However, decentralized asset trading has had the greatest impact on industries so far. Over the last two years, liquidity provision and yield farming have emerged as quite popular applications, and further segmentation of the DeFi space in the future seems justified.

Percentage of gas used by decentralized finance. Source: Glassnode Decentralized Exchanges (DEX) first gained popularity with the arrival of EtherDelta in 2017 and have been a major gas consumer since then. Since liquidity is both provided by and attracted to traders, there is a natural centralizing force in the game – at most points in time, only one or two platforms dominate this category, with Uniswap currently dominating (peaking at 88% of consumption DeFi gas, and is currently at 60%). Note also the presence of a Metamask (orange, top band) in this space, which is not directly DEX but rather an aggregator that uses the “best swap price” for the pair. This is another trend that we can expect – as the industry matures, some features may become hidden rather than overt, and users will be using the platforms that provide the most convenience.

Percentage of gas used by decentralized finance. Source: Glassnode Decentralized Exchanges (DEX) first gained popularity with the arrival of EtherDelta in 2017 and have been a major gas consumer since then. Since liquidity is both provided by and attracted to traders, there is a natural centralizing force in the game – at most points in time, only one or two platforms dominate this category, with Uniswap currently dominating (peaking at 88% of consumption DeFi gas, and is currently at 60%). Note also the presence of a Metamask (orange, top band) in this space, which is not directly DEX but rather an aggregator that uses the “best swap price” for the pair. This is another trend that we can expect – as the industry matures, some features may become hidden rather than overt, and users will be using the platforms that provide the most convenience.

Bridges, or bridges

When it comes to cross-chain, bridges are among the newest notable gas consumers. As transactions on Ethereum become quite expensive in dollar terms and as competing chains mature in terms of stability and functionality, we are seeing the emergence of interchain capital flows. In addition to the short-term jump in importance of the Ronin bridge at the peak of Axie Infinity’s popularity (peak gas consumption of 8% for several days), gas consumption by bridges has doubled over the past year (from 1% to 2%), combining the Ethereum blockchain with L2 solutions ( Polygon, Arbitrum, Optimism), as well as with competitive ecosystems (Avalanche, Polkadot).

The percentage of gas used by bridges. Source: Glassnode

The percentage of gas used by bridges. Source: Glassnode

NFT. The heyday of non-convertible tokens

Few people remember Cryptokitties today, but in 2017, the first popular NFT project briefly accounted for about a third of network bandwidth, which significantly increased network fees. In the same year, the beta version of OpenSea was released. However, it was not until the second half of 2021 that the NFT space again became significant on the gas market. Since then, it’s been a force to be reckoned with – currently about a third of all gas consumed by Ethereum is used for NFT activities. The market leader in this category is OpenSea, which consumes over 60% of all NFT-related gas.

The percentage of gas used by the activity of non-transferable tokens. Source: Glassnode A certain increase in performance was achieved thanks to the introduction of the ERC-1155 token standard, used primarily by the OpenSea Wyvern exchange – the adoption of this standard is another trend that is worth observing.

The percentage of gas used by the activity of non-transferable tokens. Source: Glassnode A certain increase in performance was achieved thanks to the introduction of the ERC-1155 token standard, used primarily by the OpenSea Wyvern exchange – the adoption of this standard is another trend that is worth observing.

Boty MEV, Miner Extractable Value

There is widespread agreement that Miner Extractable Value (MEV) is an inherent artifact of the Ethereum project and plays an important role in increasing the efficiency of the DeFi ecosystem, namely by arbitrating price differences between decentralized exchanges, accounting for over 95% of MEV activity.

The percentage of gas used by MEV bots. Source: Glassnode Contrary to what the name suggests, the main beneficiaries of MEV are not generally miners, but a community of prospectors and miners using automated tools to create MEV transactions. Miners, however, benefit from high fees associated with the urgency of arbitrage deals, which are usually winner-take-all deals, and gas is paid for well above market prices.

The percentage of gas used by MEV bots. Source: Glassnode Contrary to what the name suggests, the main beneficiaries of MEV are not generally miners, but a community of prospectors and miners using automated tools to create MEV transactions. Miners, however, benefit from high fees associated with the urgency of arbitrage deals, which are usually winner-take-all deals, and gas is paid for well above market prices.

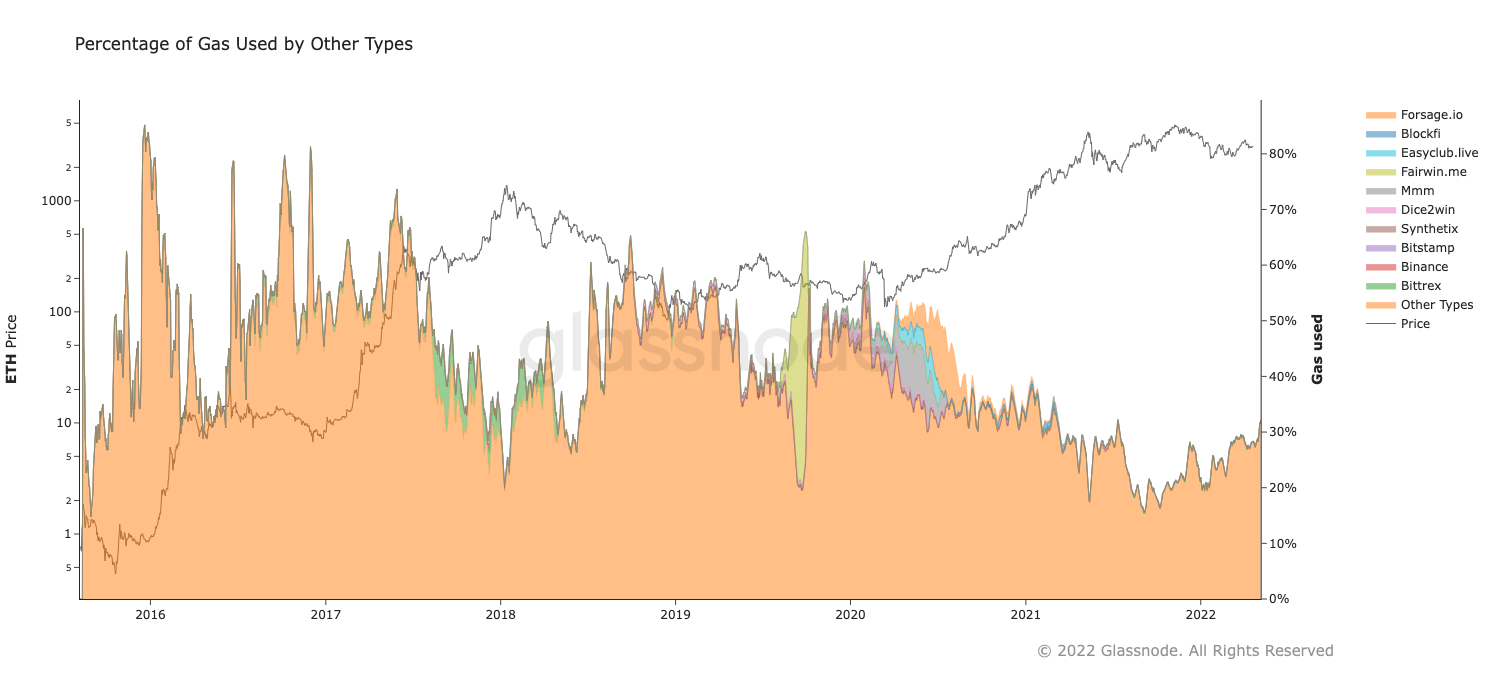

The last group in the Ethereum network, or “other”

The design of Ethereum as an unlimited platform paves the way for the identification of many other applications beyond those listed above, from on-chain games and multi-signature protocols to financial pyramids. At their peak, pyramids such as MMM (peaking at 10% gas use) and FairWin (briefly peaking at 40%) were among the most popular Ethereum use cases. It seems, however, that these times are behind us. Stock exchange contracts, especially multi-signature contracts used for fund management, are also included here. This category also includes undetected MEV mining, some DeFi protocols, and custom tokens.

Gas consumption for all other transactions. Source: Glassnode

Gas consumption for all other transactions. Source: Glassnode

Glassnode Conclusions on the Ethereum Network

Understanding the emerging dynamic ETH ecosystem is not an easy task. Value flows through the network in countless different forms, through many different channels. To make things even harder, Ethereum is increasingly connected to a plethora of other L1 and L2 chains. An ever-increasing number of assets, projects, protocols and entities exist simultaneously in multiple chains and migrate freely between platforms. – Approaching Ethereum today with the same mindset as Bitcoin, or even Ethereum in 2019, just doesn’t make sense. Relying on metrics for single assets, single chains, gives incomplete and superficial understanding – understanding the current state of the network requires vigilant awareness of new events, extensive knowledge and appreciation of nuances, comments Glassnode. Ethereum thus remains a platform primarily used for value transfer, however the scope of what constitutes value and what constitutes transfer is constantly changing. Unlike Bitcoin, Ethereum requires tools and a mindset that are use-case sensitive and adaptable, multi-entity, with a broad value definition that includes convertible and non-exchangeable tokens, etc.

The author also recommends:

Follow us on Google News. Search what is important and stay up to date with the market! Watch us >>